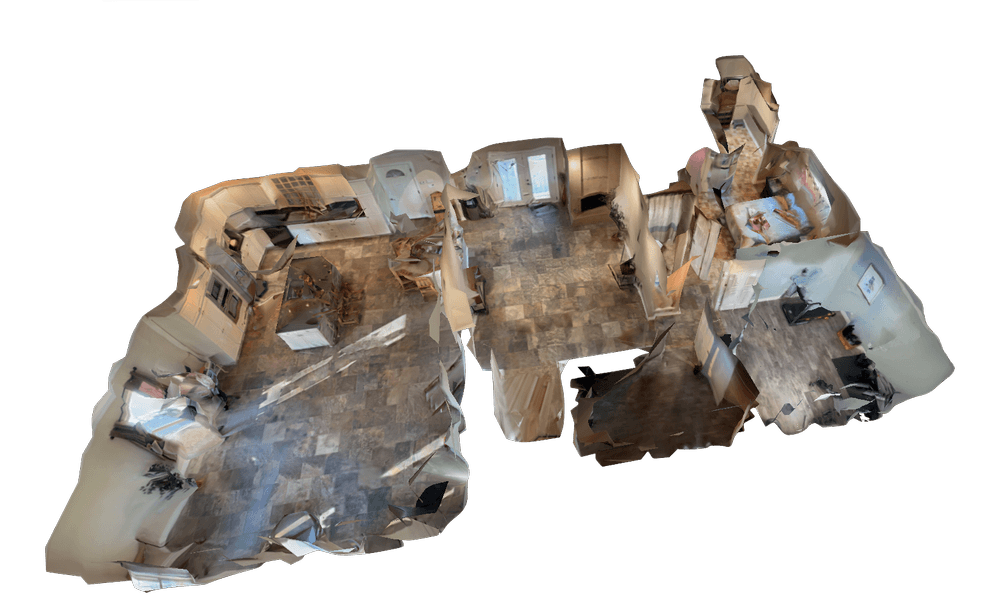

Insurance claims require defensible damage documentation and accurate loss quantification while minimizing adjuster site visits and policyholder friction. Traditional property claims workflows — field visits, manual measurements, multi-day estimate turnarounds — create bottlenecks that delay settlements and frustrate policyholders. Videogrammetry — a process that derives 3D geometry and spatial measurements from continuous video — compresses these cycles from weeks to same-day resolution by letting adjusters assess claims remotely from measurable 3D models.

Contents

- Why are insurance carriers adopting drone and video mapping?

- How does remote damage assessment work for desk adjusting?

- What accuracy levels support loss quantification and fraud detection?

- How does 3D documentation strengthen claims files and litigation defense?

- How much faster are videogrammetry-based claim cycles?

Why are insurance carriers adopting drone and video mapping?

Traditional property claims require field adjusters visiting each loss location — measuring damage, photographing conditions, and estimating repairs. That process averages 7-14 days from claim report to settlement offer. Videogrammetry lets carriers deploy policyholders or independent adjusters with smartphones to capture property damage in continuous video, upload to cloud processing, and receive measurable 3D models within minutes, according to industry workflow benchmarks from the National Association of Insurance Commissioners.

The shift from manual field inspection to video-based documentation addresses three operational pain points: scheduling delays (3-7 days to get an adjuster on-site), incomplete first-visit documentation (triggering expensive supplement requests), and catastrophe response scalability (traditional adjusters cannot cover thousands of simultaneous claims after hurricanes or hail storms).

SkyeBrowse accepts video from any smartphone, drone, or action camera via Universal Upload. Policyholders receive text message links with capture instructions — walk around damaged structures filming continuously, then upload via the mobile app. Processing happens at approximately 1:1 speed — a 6-minute property walkthrough returns a complete model in about 6 minutes on app.skyebrowse.com.

For catastrophic events — hurricanes, hail storms, wildfires — videogrammetry scales across thousands of simultaneous claims. When traditional adjusters are overwhelmed, desk-based workflows maintain service levels without mobilizing field staff. FEMA's National Flood Insurance Program reports that rapid damage documentation after flood events directly accelerates federal assistance coordination.

How does remote damage assessment work for desk adjusting?

The 3D model preserves spatial damage relationships — roof impacts, siding damage, interior water intrusion paths. Desk adjusters navigate the model interactively, measuring damaged areas, counting affected components, and applying unit pricing without physical site visits. This supports same-day initial contact and estimate delivery when policyholders report claims in the morning and carrier staff provide preliminary settlement offers by afternoon.

The workflow integrates with existing estimating platforms. LAZ point cloud exports feed into Xactimate, Symbility, and EagleView. Adjusters measure directly from 3D models, extract dimensions for material takeoffs, and generate repair estimates without field visits or manual tape measurements.

For re-inspection and supplement negotiations, carriers reference the original 3D model instead of re-deploying adjusters. When contractors dispute estimates or policyholders claim additional damage, the model provides objective evidence of documented conditions.

What accuracy levels support loss quantification and fraud detection?

SkyeBrowse offers three accuracy tiers for insurance workflows. Lite (~2-6 inch accuracy) serves preliminary triage during catastrophic events. Premium provides 0.25 inch accuracy at 8K resolution, sufficient for standard roof and siding measurements. Premium Advanced delivers 16K resolution with 0.1 inch accuracy plus AI moving object removal for disputed claims and suspected fraud investigations.

For standard property damage estimating, Premium accuracy handles roof square calculations, siding measurements, and interior damage quantification with precision adequate for Xactimate entries and settlement negotiations.

For suspected fraud — especially large commercial losses or suspicious fire claims — Premium Advanced gives SIU investigators detailed models to identify inconsistencies between claimed damages and actual evidence, supporting fraud denials and subrogation recoveries. According to the NAIC, insurance fraud costs carriers billions annually, making forensic-quality documentation a significant loss prevention tool.

How does 3D documentation strengthen claims files and litigation defense?

AWS GovCloud (US) hosting provides long-term data retention, with Premium tiers including 5-year guaranteed storage that supports claim file retention requirements and litigation timelines. Audit trails document who accessed claim models and when, establishing claims handling diligence for regulatory examinations and litigation discovery.

When coverage disputes or bad faith allegations emerge years after settlement, archived 3D models provide verifiable evidence of original damage conditions. The chain-of-custody logging and sharing controls built into Premium tiers establish data integrity for courtroom use.

Litigation exposure drops when documentation is thorough and contemporaneous. When bad faith allegations claim inadequate investigation, the 3D models and processing timestamps prove diligent handling. Subrogation recoveries also improve — detailed models provide objective evidence of failure modes and damage causation when pursuing manufacturers or contractors.

How much faster are videogrammetry-based claim cycles?

Traditional field adjusting requires 3-7 day scheduling delays, 2-4 hour site visits, and 1-2 day estimate writing cycles, averaging 7-14 days from claim report to settlement offer. Videogrammetry compresses this to same-day cycles — policyholder captures video in the morning, carrier processes the model by noon, desk adjuster writes estimate by afternoon, and settlement offers deploy within 24-48 hours of initial report.

Faster settlements reduce loss severity. When policyholders receive rapid settlements, they complete permanent repairs sooner — preventing secondary damage from weather exposure, vandalism, or deterioration. Lower severity improves combined ratios even when claim counts remain constant.

Customer satisfaction improves measurably when policyholders avoid taking time off work for adjuster visits and receive faster settlements. For adjusting operations processing 500 annual claims, the efficiency improvements generate approximately $75K-$125K in annual savings through reduced labor costs, faster settlement velocity, and supplement prevention.

For adjusters evaluating their toolkit options, see the best insurance adjuster tools guide.